It’s March 2026, and if you’ve been following tech headlines, you’ve probably seen the dramatic terms everywhere: “SaaSpocalypse,” “the great SaaS meltdown,” and even “the death of SaaS.”

Software company stocks have dropped significantly, hundreds of billions of dollars of their perceived market value have been wiped, and some investors are betting that even legacy SaaS companies won’t keep up.

So, what’s actually happening?

Software once “ate the world” - a famous idea from Marc Andreessen - taking over industry after industry. Need CRM? SaaS. Project management? SaaS. Accounting, analytics, communications? SaaS, SaaS, SaaS. SaaS companies, until recently, were seen as the biggest beneficiaries of AI - they already owned the workflows, the data, and the customer relationships. The assumption was simple: add AI on top of existing products, and growth would accelerate.

But right now the market is waking up to something different: AI isn't just boosting SaaS - in some cases, it's threatening to replace it when AI agents automate entire jobs, challenge per-seat pricing, and unbundle AI-powered development of tools. For the first time, technological progress is being viewed not just as a driver of growth, but as a potential threat to the SaaS industry itself.

But here’s the reality check: SaaS isn’t dying. It’s transforming - dramatically, and at times painfully. What we’re witnessing is the end of enterprise software as we know it - and the beginning of something potentially much stronger.

The Economic Recipe for SaaS Success and Its Achilles Heel

SaaS emerged as an evolutionary response to the inefficiencies of traditional licensed software and became the default way businesses consume software. The model was simple, measurable, and flexible - instead of high upfront costs and complex maintenance, users were offered a subscription model with regular updates, cloud access, and easy scalability. From CRM and HR systems to analytics and collaboration tools, nearly every software category shifted toward subscriptions. Companies around the world have quickly become accustomed to renting rather than owning software.

The venture market also loved SaaS for its mathematical transparency. For the past fifteen years, it seemed like an almost perfect formula: recurring revenue, predictable churn, clear unit economics. This model has fueled enormous market capitalization: Salesforce, HubSpot, Adobe, Atlassian, and ServiceNow achieved fantastic profitability through such predictable, recurring subscription payments.

However, the flip side of this economic advantage - the “subscription mechanism” - is the constant need to retain customers. As the market matures, competition increases. More players. More overlap. Less differentiation. The response is predictable: add more features, expand the product, justify the price. Over time, products get broader, heavier, and more complex.

At the same time, the economics start to shift. Customer acquisition costs (CAC) have surged significantly - often by 50–100% or more over the past five years in many segments. Retention, which used to feel relatively stable, is no longer something SaaS owners can take for granted.

These pressures don’t stay on the vendor side only, they show up in bills. To offset rising costs, companies introduce more pricing tiers, bundle additional features, and push for expansion within accounts. Software designed for broad horizontal appeal tends toward bloat: customers often pay for modules they never use, while meaningful personalization requires expensive enterprise plans or integrations - all of which drives up subscription costs even higher. As a result, many organizations manage large, fragmented stacks of overlapping tools, even as they attempt to consolidate spending.

All this creates a growing disconnect - SaaS companies need continuous expansion to sustain growth in a more expensive and saturated market, while customers, on the other hand, are pushing back on rising costs and unnecessary complexity. That gap is where subscription models start to break.

Commoditization of software

For years, companies often tolerated rising SaaS costs and growing complexity simply because there were no practical alternatives. Building software internally was expensive. It took months. It required specialized teams. And the risk of getting it wrong was high. So even if the product was bloated or overpriced, customers stayed.

Today, that equation is changing. Alongside growing pressure in the SaaS market, a new software logic is emerging. With the rise of AI and accessible development tools, businesses finally have a credible alternative - one where companies can build tailored software using AI, rather than relying entirely on subscription-based tools.

Tools like Cursor, Claude Code, and Copilot can now handle large parts of building software — generating code, structuring data, designing interfaces, and helping integrate with existing systems. For a growing number of teams, it's increasingly feasible to prototype and deploy tailored internal tools, like a custom CRM integrated with ERP and communications systems, bypassing external SaaS entirely. Not perfectly. Not always at full scale. But enough to replace or reduce reliance on external SaaS in many use cases.

As barriers to entry fall, software itself is becoming a commodity. The value of software development is depreciating with recurring licensing becoming unreasonable. Instead of paying indefinitely, companies start to think in terms of one-time, targeted creation. In that sense, software begins to shift back toward being a capital asset - something companies own and control, not rent indefinitely.

AI-powered generation also solves the problem of standardized, one-size-fits-all software. Systems analyze specific use cases, processes, and data, then output lightweight, specialized tools without bloat, delivering higher performance, lower dependency, better fit and an easier management.

All this has massive implications for SaaS positioning. Such democratization of software development leads to proliferation of numerous alternative options, driving down prices and eroding the perceived value of many SaaS offerings. Users can replicate not just core functions but entire add-on ecosystems that vendors would sell to grow revenue from existing customers. Besides, customers now hold the ultimate negotiation lever: if a vendor's pricing or terms don't align, they can explore building alternatives - or simply threaten to. Even if they do not take the build route, the whole possibility of such an alternative creates relentless downward pressure on renewals, expansions, and contract terms, forcing vendors to justify every dollar deeper, harder-to-copy differentiation - not just feature lists.

End of per-seat SaaS pricing in the era of AI agents

Even if companies continue using SaaS, AI is creating a new kind of pressure for vendors. Most SaaS products are essentially a structured interface on top of data. CRM stores deals. Helpdesk stores requests. The task manager stores tasks. Accounting stores transactions. The user manually enters information, the system structures it, and then generates reports. Even major players like Salesforce, Notion, Monday.com, and others, despite the complexity of their ecosystems, remain within this logic: form - database - report - subscription. This model worked perfectly well in the era when humans were the primary data controllers and human labor was required to support those interfaces. The more employees you had, the more seats you needed.

The more seats, the more revenue for SaaS.

AI starts to break that equation. Instead of humans being the primary interface with software, that role is increasingly shifting to AI agents. And that creates a fundamental problem for SaaS pricing. You don’t need 50 seats if one agent can handle the workload. You might not even need 10. Value starts to decouple from headcount. Productivity goes up, but seat count goes down. And that hits directly at SaaS revenue.

In 2026, this isn't hypothetical. Across the market, per-seat pricing is already starting to weaken. More companies are experimenting with hybrid models, usage-based pricing (tokens, workflows, transactions), and even outcome-based pricing (per resolution, per task completed). Some vendors are trying to adapt by redefining what a “seat” is - for example, pricing AI agents as premium users.

But that doesn’t fully solve the problem. The core assumption behind SaaS - that revenue scales linearly with the number of users - is no longer stable. And once that assumption breaks, the entire pricing model has to be reconsidered. SaaS companies are no longer just optimizing for more users. They have to rethink what they’re actually charging for. Access is no longer enough. Usage is changing. And outcomes are becoming the only thing that’s hard to replace.

Market Reality in 2026

Yes, headlines are full of drama like "SaaSpocalypse" or "2026 SaaS crash" - software stocks took hits, valuations compressed. But the data tells a different story: this isn't AI killing SaaS. It's a painful re-rating after years of easy growth, plus budget shifts toward AI investments and infrastructure.

The global SaaS market still continues to grow. It is projected at around $465 billion in 2026 (up from ~$408 billion in 2025), per Precedence Research and Zylo's 2026 stats roundup with long-term projections still pointing toward a $800B–$1T+ market. North America still leads (~46–47% share), but places like APAC are growing fastest.

What has changed is the pace. Growth has slowed compared to the 2020–2023 period, when SaaS companies were expanding at 25–30% annually. Today, growth rates have normalized closer to the mid-teens. The market is no longer in a hyper-expansion phase - it’s maturing.

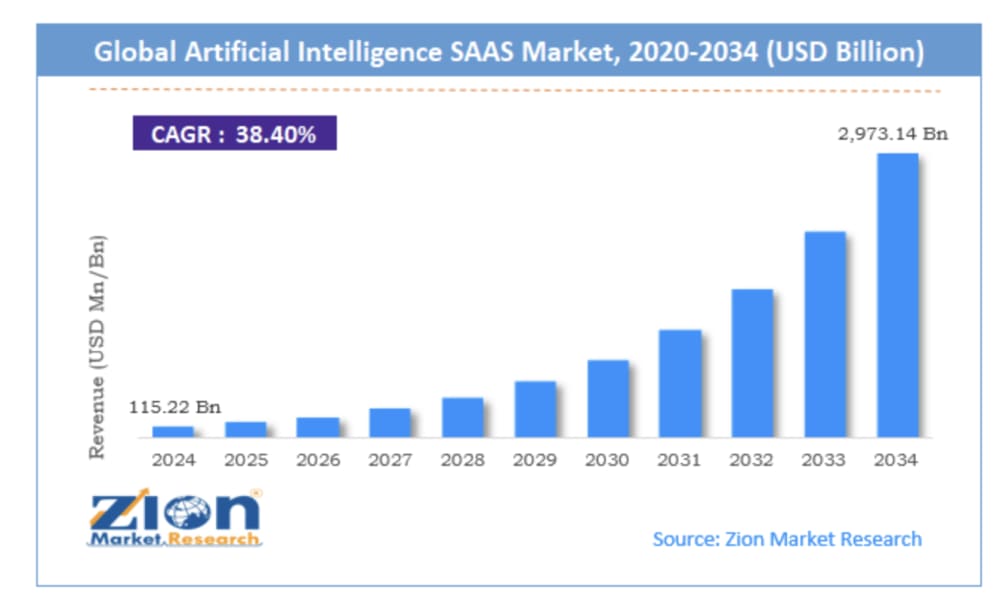

At the same time, AI-driven software is growing significantly faster. AI-powered SaaS segments are expanding at 38%+ CAGR, becoming a major driver of new value creation in the industry.

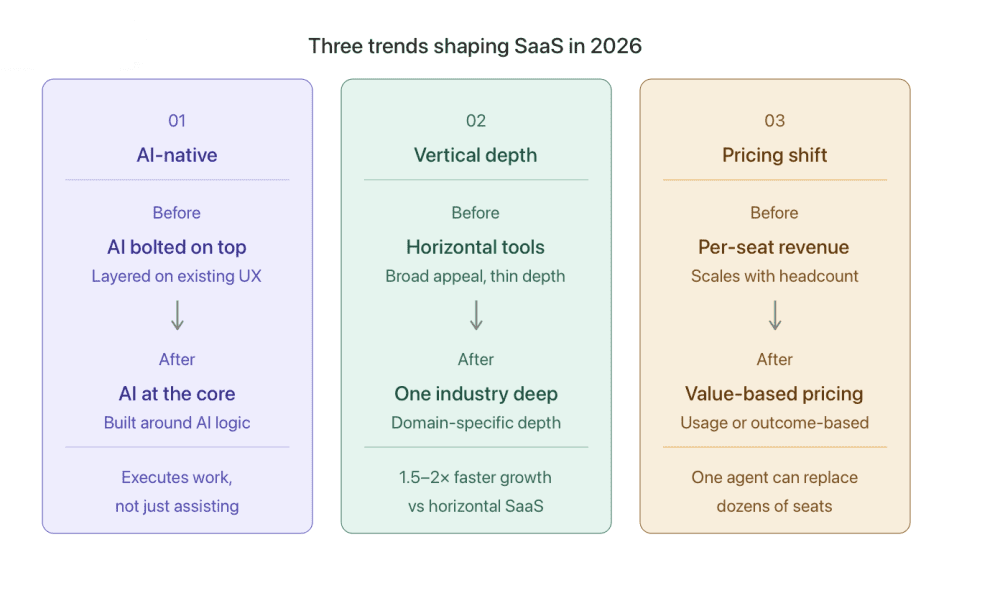

So the reality is more nuanced: the SaaS industry is being reshaped. Capital is shifting. Growth is becoming harder. And value is moving toward companies that can integrate AI effectively, rather than rely on the traditional subscription model alone. As a result, a new set of trends is emerging - ones that are already defining which SaaS companies succeed in 2026.

1. AI-native instead of AI bolted on

AI is no longer just improving software - it is changing what software does. Traditional SaaS gives users tools to do work. Products with AI bolted on follow the same logic: an existing workflow with AI features added to specific surfaces - a “summarize this” button, an AI-generated draft, a chatbot in the corner. The core product logic remains unchanged. AI is a feature layer on top.

AI-native SaaS is different. It does the work for the user. Instead of managing a CRM, configuring workflows, or analyzing dashboards, users rely on systems that execute tasks, make decisions, and adapt in real time. This shift is driven by the rise of AI agents. What started in 2024–2025 as copilots and assistive features is becoming production-ready systems in 2026 - agents that can operate across tools, orchestrate workflows, and handle multi-step processes with minimal human input.

New AI-native leaders no longer offer clients "buy a subscription and set everything up themselves." They sell finished products - closed financial reports, verified contracts, or processed client requests. The AI-native product delivers more value, replaces both human labor and manual software work, and can price competitively while maintaining healthy margins over time.

If you're early enough in your build, the question is: are you adding AI to your product, or are you designing your product around what AI makes possible? These are genuinely different starting points and they lead to different products.

2. Deep Verticalization

Buyers want tools that understand their exact workflows and regulations. Horizontal SaaS - tools built for anyone, solving a general problem - is harder to build competitively simply because it can’t match the depth and specificity of industry-focused solutions.

When you build for a specific industry or professional context - field service management for HVAC companies, compliance tooling for staffing agencies, project management for architecture firms - your advantages compound in ways that horizontal tools can't replicate. You understand the workflow deeply. Your terminology matches your users' terminology. Your integrations are with the three or four systems your vertical actually uses, not the fifty systems a general tool has to support. And critically, your data becomes increasingly valuable and specialized as you grow. Think of it this way - a general CRM is useful to 10,000 companies. A construction-specific CRM (with project scheduling, labor cost tracking, and compliance built in) solves 80% of problems out of the box for a builder.

The founders winning right now picked a vertical and went uncomfortably deep before thinking about going wide. Uncomfortably deep means: early customers feel like you built this specifically for them, not for "companies like them."

While horizontal SaaS is still larger than vertical. The latter starts from a smaller base (~$95–157B range in 2025–2026 estimates) but is growing noticeably faster. CloudNuro report suggests Vertical SaaS in key industries (healthcare, fintech, construction, logistics, etc.) is growing at 22–28% annually, compared to horizontal platforms at 14–17%). So, the trajectory is clear. Vertical is where capital and founders are flowing.

3. Pricing Evolution - From Seats to Value-Aligned Models

Seat-based pricing made sense when software was used by individual humans sitting at desks. It's increasingly awkward in a world where AI agents, automated workflows, and background processing do meaningful work without any human "sitting" in the product. One agent can replace dozens of seats, so founders building automation-heavy or AI-driven products and still pricing per seat are creating a structural mismatch: the value delivered scales with usage, but the revenue doesn't.

Hybrid models are the bridge most companies use first (and the current winner). It’s possible to keep a predictable base subscription (platform fee or limited seats for access/governance) + add a variable layer (usage or outcome). It gives buyers budget certainty while letting vendors capture upside from heavy AI usage.

Usage-based pricing is where customers pay for what they consume, not how many accounts they have. It has been growing for years, but 2025-2026 is when it crossed from "interesting alternative" to "table stakes for AI-native products." Outcome-based pricing is the more ambitious version of this shift. Instead of charging for seats or API calls, you charge a percentage of the value delivered - cost savings, revenue generated, time recovered. It's harder to implement and requires tight instrumentation of your product's actual impact, but it aligns incentives in a way that both founders and enterprise buyers are increasingly motivated by.

Thus, seat-based SaaS isn't dead, but it requires justification now that it didn't before.

If you're at the pricing design stage, be honest about what unit of value your product actually creates and whether your pricing model reflects that. If agents do the heavy lifting, shift toward hybrids or usage/outcome to avoid seat compression pain and unlock growth. Start small (add a usage tier to existing seats), test with early customers, and iterate.

Bottom Line: Beginning or End of SaaS?

The core SaaS model - solving real business problems and earning recurring revenue through ongoing relationships is not going away. Unit economics are still some of the best in business when executed well. But the era of “easy SaaS”, where you could find a gap, build something decent, and grow through distribution, is probably over. App fatigue is real. AI agents are quietly questioning the entire logic of per-user licensing. And CIOs are drawing a clear line in the sand: “No more tools.” But it is very much the beginning of the AI-native SaaS era. This is where the real opportunity begins. SaaS isn’t dying. It's evolving into something bigger and better, powered by AI. For founders who understand this and build accordingly, 2026 is genuinely a strong moment. If you're building, investing, or running a SaaS business, the message is clear: double down on AI-native architecture, vertical depth, and usage-based models now.